Governance is a control mechanism. Whoever holds governance rights can propose changes, vote on others’ proposals, and implement decisions on the platform. Companies call this the Board of Directors. Crypto is more complicated.

You can use crypto without touching governance at all. Coinbase is a centralized exchange with a traditional board structure. VISA processes crypto payments. Starbucks accepts them. None of those users have governance rights. Centralized organizations follow a hierarchical structure regardless of whether crypto is involved.

Public blockchains work differently. They are decentralized networks where anyone can participate in decisions. In practice, that participation mostly happens through technical developer communities who review code and propose changes. The applications built on top of a blockchain can have their own separate governance systems entirely.

Types of Governance In Crypto

Just like there are many consensus mechanisms, there are different ways to govern crypto platforms. Sometimes it’s better to have more than one governance type, and sometimes none. Governance can be on-chain or off-chain:

On-Chain Governance

In on-chain governance, smart contracts determine decisions based on the community’s approval. Smart contracts are autonomous functions of code that implement proposals once there are enough votes. The way of voting is similar to staking, except the votes are called governance tokens.

Platforms based on on-chain governance are called Decentralized Autonomous Organizations (DAOs). Joining a DAO is available to everyone, but to have governance influence, you need governance tokens:

- DAOs require a minimum token amount to submit proposals (e.g., 2.5M UNI in Uniswap or 50 AAVE in Aave)

- After you submit the proposal, there’s a voting period for members to approve or reject it. To be successful, it needs to cross a certain token limit within that time with a reasonably low number of votes against it.

- After the voting period, successful proposals will apply to the protocol in the next update.

Even then, no proposal is final. Users can suggest anything, like removing previously added features if the community agrees.

Off-Chain Governance

What about off-chain governance? The most obvious benefits are:

- There are no token minimums, so anyone can submit proposals.

- There are no governance tokens, so there’s no weighted voting.

Because it’s so accessible, there are more proposals that could compromise the blockchain’s security. That’s why there are dozens of development experts moderating these proposals. Here’s Ethereum’s off-chain governance as an example:

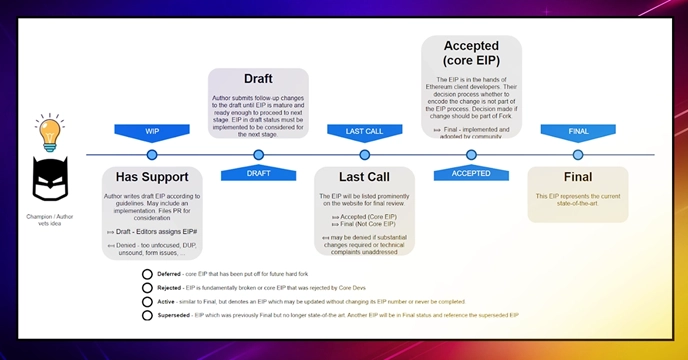

- First, you submit a proposal (EIP)

- You can then publish it as a draft, and the editors will check the formatting so it’s consistent with all other EIPs. They will point out those errors, and once corrected, you can publish the EIP officially for peer review.

- Ethereum Editors, core developers, and the most active members have two weeks to review, make questions, and request changes (AKA “last call”). If everything is resolved within that time, it switches from Last-Call to Final (Non-Core) status.

- Then, the core developers decide whether to approve the proposal for the next fork (Final Core), reject it, delay it, or ignore it.

- If your proposal reaches this stage, it should appear on the list of accepted EIPs on the next fork announcement.

Thus, the core dev teams have the final say on what to change. It’s not enough to make proposals secure and error-free. They have to align with the Ethereum vision and efficiency goals.

Which doesn’t sound very decentralized. After +5,000 EIPs published in ten years, less than 10% were approved (if not replaced).

Governance Models Compared: Which One Fits Your Project?

Not every project needs the same governance structure. The table below maps each model to its real costs, control tradeoffs, and best-fit use cases.

👉 Quick takeaway: On-chain DAO governance maximises community participation but carries the highest collusion and regulatory risk. Off-chain governance keeps control with expert reviewers and has the lowest regulatory exposure. Governance-free (immutable) protocols trade flexibility for predictability. Hybrid models sit between the two extremes.

| Model | Who Decides | Token Requirement | Collusion Risk | Regulatory Exposure | Best For |

|---|---|---|---|---|---|

| On-Chain (DAO) | Token holders via smart contract |

⚠️ Yes e.g. 2.5M UNI to propose |

🔴 High without safeguards |

🔴 Medium-High SEC 2026 scrutiny on governance tokens |

DeFi protocols with large, active communities 🏆 Most participatory model |

| Off-Chain (EIP / BIP style) | Core dev teams after open review | 🟢 No |

🟢 Low Expert gatekeeping |

🟢 Low No token sales involved 🏆 Lowest regulatory exposure |

Base-layer blockchains like Ethereum and Bitcoin 🏆 Best for base-layer protocol security |

| Hybrid (On + Off-Chain) | Token holders + expert review layer | ⚠️ Yes, lower thresholds | ⚠️ Medium | ⚠️ Medium |

Mid-stage protocols balancing speed and security 🏆 Best balance of participation and oversight |

| Governance-Free (Code-Only) | No one — rules are immutable | 🟢 None |

🟢 None 🏆 Zero collusion risk |

🟢 Low |

Stable, finished protocols where predictability beats flexibility 🏆 Best for censorship resistance and predictability |

How to Choose: A 3-Question Framework

- Is your protocol still evolving? If yes, you need governance. If it runs without incidents and changes would introduce risk, governance-free may be the better call.

- How large and active is your community? On-chain governance works when thousands of holders are engaged. Fewer than a few hundred active participants usually means a small group will dominate votes anyway.

- Are your governance tokens also used for trading or yield farming? If yes, conflicts of interest are likely. Separating governance tokens from utility tokens reduces the risk that market dynamics override community decisions.

The SEC’s 2026 exchange registration framework adds a fourth question for projects operating in the US: does your governance token qualify as a security under the new interpretation? If it does, on-chain governance design will need to account for investor-protection requirements and custody standards.

How Exactly Does Governance Work With Blockchains?

Even decentralized governance has its limits when changing the rules. The developers of a protocol can design what can or shouldn’t be changed (in case the community proposes it). But what if your improvement proposal is outside of that scope?

In 2016, a barrage of DoS attacks was threatening Ethereum. They could have played by the rules and left the network at high risk (which created Ethereum Classic). Instead, they stopped those threats with the DAO fork. A (hard) fork is an alternative blockchain that inherits the original blocks but follows new rules to continue the chain.

Blockchains are immutable and unique, a bit like collectibles. While you can “copy” the Mona Lisa or create a modified painting, people still recognize the original. When the blockchain doesn’t allow a certain change, the governance creates a new chain division.

Ethereum has gone through more than 20 protocol upgrades since its 2015 launch. Paris was the upgrade that merged proof-of-work with proof-of-stake in 2022. Since then, Shapella (2023) enabled staking withdrawals, and Dencun (2024) introduced proto-danksharding to reduce Layer 2 fees.

The newest version is the official one for the same reason it has always been: the community adopted it. Decentralized governance cannot force nodes to update. Each of the 400,000-plus peers updates voluntarily, and once enough do to guarantee security, the new version becomes the main chain.

The Problems Of Governance in Crypto

Decentralized governance isn’t any easier than traditional governance. How do you make a fair, rewarding system where people want to participate? How do you avoid concentrating power on the biggest contributors? How do you deal with those who disagree on decisions?

The first iteration was MakerDAO in 2014, so you would think that we’d have these answers by now. But like the blockchain trilemma, governance choices are subjective. At least three problems lead to its manipulation:

- Members don’t participate. The entry barrier is too high, discussions are too technical, there aren’t enough incentives, maybe they don’t even know that governance exists, or they’re happy with the current platform, or they don’t believe that they can change anything (AKA political apathy). While there are countless reasons for low participation, the consequences are the same: high centralization, and low security.

- DAOs over-prioritize token holdings. If you get proportional governance power for every token you buy, the biggest buyers will dominate. While they may not dump the project, they can change rules in their favor and discourage smaller members from joining. Decentralization should involve probability, history length, locations, and more besides token quantity.

- Most governance tokens are not standalone. They double as utility tokens for liquidity provision, yield farming, or fee sharing. When the same token governs the protocol and generates yield, large holders have a financial incentive to vote in ways that protect their returns rather than the community’s long-term health. The markets do not just influence the platform. Under token-weighted voting without separation safeguards, they can control it. The 2026 SEC securities law interpretation adds another layer: governance tokens with profit-sharing features face a higher risk of being classified as securities, which would trigger compliance requirements the protocol may not be designed to meet.

At first, these choices may speed up development and bring more investors. But you’re not building a community, only attracting traders. Eventually, governance loses participation as members switch to more competitive, welcoming platforms.

What Really Makes Governance Work

Few platforms have succeeded in decentralized governance. While there are hundreds of DAOs, most have below 100 active users and a dozen votes per proposal. The most popular have been Uniswap, Aave, ENS, Curve, and PancakeSwap.

Here’s what the top 5 have in common:

- They’re user-friendly. How easy is it to swap tokens on Uniswap? That’s how easy it is to vote. You connect your wallet, click on “Vote,” select an active proposal, vote for or against, select the amount, and confirm the Metamask contract (after the voting results, the tokens return to your wallet). And you don’t need to know tech jargon like on Ethereum. The proposals you’ll find are simple: add dApp to blockchain X, change X fee, contribute treasury funding to X, or integrate with another app.

- There’s both on and off-chain governance. There are informal discussions, but there aren’t core developers regulating proposals. There are governance tokens, but new proposals have lower requirements.

- They prevent centralization. You can only vote with the governance tokens you had up to a certain Ethereum block number (if you buy more after, it won’t increase voting power). Proposals also need majority votes over 50% and participation from at least 5% of all holders.

These also happen to be competitive platforms with high utility, which isn’t a coincidence. Why participate in an inactive project that’s mediocre or a copy of a better one? After all, the governance incentive isn’t to get free money but a better platform you already like

How Regulations Are Reshaping Crypto Governance

For years, the assumption was that decentralized governance existed outside the reach of securities law. That assumption is now wrong.

In March 2026, the SEC finalized its Cryptocurrency Exchange Registration Framework. It requires crypto exchanges to meet investor-protection standards, establish a Technology Standards Office for custody solutions, and pass annual penetration testing. Governance structures that control treasury funds or protocol fees now sit inside that regulatory perimeter.

A week later, the SEC issued Rule Release 33-11412, clarifying how federal securities laws apply to specific crypto assets and transactions. The release draws a clearer boundary between assets that are securities and those that are not. For DAO governance token holders, this matters. If a governance token is classified as a security, the mechanics of how it is issued, traded, and used to vote may require compliance steps the protocol was not designed for.

The SEC and CFTC are now aligned on market structure. Bipartisan legislation in the Senate is moving in the same direction. This is not a future risk. It is the current environment.

What this means for DAO governance design:

- Governance tokens with profit-sharing or yield components face the highest securities classification risk.

- Protocols that separate governance tokens from revenue-generating utility tokens reduce that exposure.

- DAOs with treasury controls above a certain scale may need to document governance processes to satisfy custody and audit requirements under the new framework.

- El Salvador’s LEAD framework, which already brought exchanges like Bitso under formal regulatory scope in May 2026, is an early example of how national regimes are integrating crypto governance into public compliance law.

The PwC Global Crypto Regulation Report 2026 tracks these developments across jurisdictions. The regulatory picture varies significantly by country, but the direction is consistent: hybrid governance (code plus legal compliance layer) is replacing the assumption that code alone is sufficient.

Collusion, Capture, and the Limits of Token Voting

Token-weighted voting has a structural problem. The more tokens you hold, the more votes you control. That sounds fair until you realize a single actor with enough capital can buy a majority stake and pass proposals that benefit only them.

This is called governance capture. It is not theoretical. Empirical research published in 2023 documented the hidden shortcomings of real DAOs, finding that voting power in most protocols concentrates in a small number of wallets. A 2026 paper in ScienceDirect went further, modeling collusion-proof DAO mechanisms and identifying specific design features that reduce the attack surface.

The mitigations that current research supports:

- Time-locked voting weight: voting power is based on tokens held at a snapshot block, not current balance. Uniswap already uses this. It prevents last-minute whale purchases from swinging votes.

- Quorum floors with participation minimums: Uniswap requires more than 50% approval and participation from at least 5% of all token holders. Small cartels cannot pass proposals in low-turnout votes.

- Separation of governance and utility tokens: when the same token governs the protocol and generates yield, large holders have financial incentives to vote in ways that protect their yield, not the community.

- Governance analytics dashboards: new multi-chain KPI frameworks (published in May 2026 via SSRN and ResearchGate) track participation rates, proposal pass rates, wallet concentration, and treasury health across chains. These dashboards make governance attacks visible before they succeed.

Collusion-resistance is now a design requirement, not a nice-to-have. Any protocol launching governance in 2026 without these safeguards is building on a known vulnerability.

Metagovernance: When DAOs Vote on Other DAOs

Most governance discussions focus on a single protocol. But some of the largest DeFi ecosystems now hold governance tokens in other protocols. That creates a new layer of influence called metagovernance.

Here is how it works. Protocol A holds a large position in Protocol B’s governance token. Protocol A’s community can vote on how Protocol A uses that position, which in turn influences Protocol B’s outcomes. The governance of one DAO flows through into the governance of another.

ArXiv research published in 2026 mapped the on-chain and off-chain mechanics of DAO-to-DAO voting in detail. The findings show that metagovernance is already active in major DeFi ecosystems. It is not an edge case.

Why this matters in practice:

- A DAO with a large treasury can accumulate governance tokens in competing or complementary protocols and steer their development.

- Small token holders in Protocol B may not realize that a significant portion of voting power is being exercised by Protocol A’s community, not individual humans.

- Metagovernance coordination can be legitimate (two DAOs aligning on a shared upgrade) or adversarial (one DAO using another’s governance to block a competitor’s proposal).

For anyone participating in DAO governance today, the practical takeaway is simple. Check who holds the largest voting blocs. If a significant share is held by another protocol’s treasury, the governance dynamics are more complex than they appear on the surface.

How to Measure Whether a DAO’s Governance Is Actually Working

Most people evaluate a DAO by its token price or TVL. Neither tells you whether governance is healthy.

Researchers publishing in May 2026 via SSRN and ResearchGate proposed a multi-chain KPI dashboard framework specifically for DAO governance health. The framework tracks three categories of metrics across chains:

Participation health:

- Voter turnout rate per proposal (number of unique wallets voting divided by total eligible holders)

- – Proposal submission rate (how many proposals are submitted per quarter)

- – Repeat voter ratio (what share of voters participate in more than one proposal)

Treasury health:

- Runway in months at current spend rate

- Share of treasury held in the protocol’s own token versus stablecoins or diversified assets

- Treasury diversification score

Governance velocity:

- Average time from proposal submission to final vote

- Proposal pass rate over the last 12 months

- Number of implemented proposals that were subsequently reversed

Why these numbers matter: a DAO with a 2% voter turnout, 90% of treasury in its own volatile token, and a 6-month average proposal cycle is structurally fragile regardless of its TVL. These KPIs make that fragility visible before a governance attack or treasury crisis occurs.

For a project you are evaluating or participating in, you can pull most of these numbers from on-chain data using tools like Tally, Boardroom, or Snapshot’s analytics views.

Is Governance In Crypto The Only Answer?

Governance makes protocols flexible and allows vulnerabilities to be patched quickly. That is genuinely valuable. But it comes with real tradeoffs, and the tradeoffs are now more concrete than they were in 2023.

Off-chain governance concentrates final authority in core developer teams. On-chain governance concentrates power in the largest token holders. It takes thousands of tokens to submit a proposal on most platforms and only a few million dollars in purchases to achieve a voting majority on smaller DAOs. Neither model is fully decentralized in practice.

Regulation adds a third dimension. The SEC’s 2026 securities law interpretation means that governance is no longer just a design choice. For protocols operating in regulated jurisdictions, it is also a compliance question. A governance structure that made sense in 2021 may now create securities law exposure that the original designers never anticipated.

Governance-free protocols avoid all of this. If a protocol runs as intended without needing changes, immutable code eliminates governance risk, regulatory surface area, and the attack vectors that come with token-weighted voting. Liquid Loans is governance-free. That design choice creates a predictable environment for stability pools, borrowing, and lending without the overhead of managing a DAO or navigating evolving securities rules.

FAQ

Are DAOs and governance the same?

Not exactly. Governance is the broader category. DAOs are one implementation of on-chain governance, not the only one.

Blockchains use off-chain governance (EIPs, BIPs, core developer review). DAOs are protocol-level dApps with on-chain or hybrid governance. There is no ‘Ethereum DAO’ because Ethereum’s governance runs through its developer community, not a smart contract voting system.

The most active DAOs by proposal volume include Uniswap, MakerDAO, and Aave. But the regulatory environment is shifting. Under the SEC’s 2026 securities law interpretation, DAOs that issue governance tokens with economic rights may face securities compliance requirements. Not all platforms use DAOs, and governance-free designs sidestep this exposure entirely.

What is the governance of Ethereum?

Ethereum has off-chain governance in the way of Ethereum Improvement Proposals (EIPs) and informal forum discussions. Developers can suggest new code features and send them for reviews based on an EIP template. The proposal goes through multiple statuses for weeks, from revisions to the approval of core teams.

While anyone can submit EIPs, only these teams can include them in upcoming forks. They consist of a few members from the Ethereum Foundation and Community. When accepting EIPs, they can be deferred (reserved for future consideration) or final (intended for the next upgrade). Still, the community can sometimes remove old EIPs after a closer review.

Does Bitcoin Have Governance?

Not only has Bitcoin governance, but it’s similar to Ethereum’s. It consists of over a hundred core developers from different organizations. Users can suggest improvements via Bitcoin Improvement Proposals (BIPs), which these teams then review.

Unlike Ethereum, Bitcoin’s updates are only backward compatible (soft forks). The most important upgrades were SegWit in 2017 and Taproot in 2021.

Are governance tokens and liquidity tokens the same?

They might seem the same as they both involve locking a token amount. The more you stake, the more governance or liquidity tokens you get. While they have different utilities, they’re both based on proof of ownership.

Governance tokens grant voting power, and they’re proportional to what you’ve staked. Liquidity tokens are a receipt of the coins you provided to a liquidity pool. While you can sell these tokens for profits, you can’t redeem your initial deposit without them. But you can yield-farm with liquidity tokens while earning interest from the staked amount.

How do the SEC’s 2026 rules affect DAO governance?

The SEC finalized its Cryptocurrency Exchange Registration Framework in March 2026 and issued Rule Release 33-11412 clarifying how federal securities laws apply to specific crypto assets. For DAOs, the key question is whether the governance token qualifies as a security. Tokens that carry profit-sharing rights, dividends, or yield features face a higher classification risk. If a governance token is classified as a security, the DAO may need to register with the SEC, restrict token transfers to accredited investors, or restructure how voting rights are allocated. The SEC and CFTC are now coordinating on market structure rules, and bipartisan Senate legislation is in progress. Protocols that have not reviewed their governance token design against the new interpretation should do so before issuing new tokens or expanding governance rights.

What is metagovernance in crypto?

Metagovernance happens when one DAO holds governance tokens in another protocol and uses them to influence that protocol’s votes. Protocol A’s community can vote on how Protocol A deploys its position in Protocol B, which effectively gives Protocol A a voice in Protocol B’s governance decisions. Research published on arXiv in 2026 documented the mechanics of DAO-to-DAO voting in live DeFi ecosystems. For token holders, the practical implication is that the largest voting blocs in a DAO may not be individual users. They may be other DAOs pursuing their own strategic interests.

Connor

Connor is a US-based digital marketer and writer. He has a diverse military and academic background, but developed a passion over the years for blockchain and DeFi because of their potential to provide censorship resistance and financial freedom. Connor is dedicated to educating and inspiring others in the space, and is an active member and investor in the Ethereum, Hex, and PulseChain communities.